RSS

RSS| Autorius | Žinutė |

2010-10-11 14:23 #146967

4 4

|

|

|

http://www.ecb.int/press/pr/date/2010/html/pr101009.en.html

nuo vakar Didžiajam Lombarde(ECB) naujos taisyklės (tinka nebe viskas ir nebe visi): 1) Asset-backed securities (ABSs): clearer and more stringent provisions on the cash flow-generating assets backing ABSs, identifying swaps and synthetic securities as non-eligible cash flow-generating assets. In addition, in order to reduce claw-back risk with a view to limiting credit and legal risks, the amended provisions include restrictions on the geographical scope of ABS originators and the underlying assets to the European Economic Area (EEA), 2) Close links: the introduction of additional exemptions from the prohibition of close links. It relates to non-UCITS covered bonds that fulfil all criteria that apply to asset-backed securities, and are both backed by residential real estate loans and denominated in euro. 3)Discretionary measures: the enhancement of the formulation regarding the suspension, limitation or exclusion of counterparties and assets on the grounds of prudence or a default. 4)Collateralisation non-compliance: consistency between the treatment of cases where the counterparty fails to sufficiently collateralise a liquidity-providing operation on the settlement day, and cases where the counterparty fails to sufficiently collateralise the operation during the life of the operation. nebedaug beliko tinkamo ir dar neatnešto... |

|

| 2010-10-14 12:05 #147837 | |

|

2010-10-15 13:37 #148082

2

|

|

|

http://www.eurointelligence.com/index.php?id=581&tx_ttnews[tt_news]=2925&tx_ttnews[backPid]=901&cHash=1a5a743e3c

adrese yra lauztiniu skliaustu [] - tai link'as neveikia, bet copy-paste budu turetu atidaryti straipsnis vadinasi: "Is Belgium next?" |

|

|

2010-10-15 15:41 #148121

3

|

|

|

o cia apie prekybos karu uzuomazgas "vieningoje" Europos rinkoje:

"The true spirit of the single market" The French industry ministry claimed yesterday that Eurostar was only allowed to use French-made trains, not the German trains the Eurostar company had recently ordered, on the grounds that only French trains meet the safety standards. The FT has this hilarious story, including this quote from the minister: “Since the beginning we have told the management of Eurotunnel, which manages the tunnel, and Eurostar, which operates it . . . that material other than Alstom material cannot be used.” FT Deutschland even leads with the story, and talks about an escalating conflict between Paris and Berlin, and a symbol of rising protectionism. |

|

|

2010-10-20 11:15 #148978

5

|

|

|

http://pragcap.com/problem-depression-margin-compression

1) Serious economic downturns all have in common margin compression — where the change in the price level of raw inputs and unleveraged assets rises relative to the price level of finished goods and leveraged assets. While many consider the great depression of the 1930s to have been a deflationary event (and it surely was) it is instructive to note that commodities deflated by far less than finished goods, and those by far less than the value and income generated by financial assets. What made the economy of the 1930s so destructive was the inability of businesses to sell products in any meaningful quantity at prices that covered their cost of manufacture. by devaluing the currency and encouraging speculation in raw inputs, FED has raised the operating costs of the private sector (households and businesses alike) significantly within the dollar economy. In short, the FED seems to have become a vehicle of margin compression and profit destruction — increasing costs relative to revenues, reducing income, amid a deleveraging cycle. If this policy is pursued further, we may well see margins compress further as commodity prices rise relative to all else while income stagnates or falls, driving huge numbers of private sector participants cash-flow negative and into bankruptcy corporate bond market largely refinancing to cut down the income stream to creditors. p.s. zodziu visur tas pats- pinigu srautai traukiasi refinansuojant mazomis palukanomis arba bankrutuojant. Vyksta Didysis turto perskirstymas: is vidurine klases i banku balansus (makro politiniu masteliu: is vidutinio dydzio valstybiu be monetarines politikos i didziuosius centrus) p.p.s. VZ rase, kad Rockfeleriai Europoje ikure NT fonda, is banku didmena supirkinesianti "distressed property". musu bankai nuosekliai ji pakuoja, o imones supakuos vyriausybe. idomu tik kaip pirks uz tuos bevercius zalio tualetinio popieriaus rulonus |

|

| 2010-10-20 20:45 #149179 | |

|

O tuo tarpu Amerikoje...

(Kiek senstelėjusi naujiena) O "Amerikoje" sprogsta didžiulis skandalas dėl Foreclosure teisinių procedūrų pažeidimų ir dokumentų klastojimo. Visos 50 valstijų sustabdė namų atėmimo iš skolininkų procesą. Yahoo Finance! praneša: States' Probe of Foreclosures Could Force Reforms A joint investigation by every state and the District of Columbia could force mortgage companies to settle allegations that they used flawed documents to foreclose on hundreds of thousands of homeowners. It could take months, at least, for any settlement to be reached. But legal experts say lenders could be forced to accept an independent monitor to ensure they follow state foreclosure laws. The banks could also be subject to financial penalties and be forced to pay some people whose foreclosures were improperly handled. For banks, "the most efficient way for them to get out from under this to settle across the board," said Kathleen Engel, a law professor at Suffolk University in Boston. |

|

|

|

2010-10-20 20:49 #149181

1

|

|

siaures vejau,kai tuos nt paketus pirks,zalias popierelis bus all time high

|

|

| 2010-10-20 21:01 #149192 | |

|

Skeleton, koks sutapimas, visa tai vyksta prieš rinkimus.

Natural born loser.

|

|

|

2010-10-21 16:02 #149392

3

|

|

|

pasirodo ir ETF's galima frakcinio rezervo principa panaudoti

citatos butu ilgokos, bet susipazinti su industrijos virtuve manau butina. Juolab kad pensiju fondu ir mum&dad investuotoju, ETF'ais uzsikrovusiu, visose salyse yra daugybe: http://ftalphaville.ft.com/blog/2010/09/18/346406/can-an-etf-collapse/  p.s. komentaruose radau trumpai ir aiskiai: 1) Mutual funds actually own the underlying shares on the buyers' behalf. ETFs own some of the underlying shares and depend on various unknown counterparties and brokerage margin standards to promise to buy the rest in the future, should they be needed. That is very different from what most buyers of ETFs believe they own. 2) Most people don't fret over the distinction between bank deposits and cash-in-hand, just as most stock traders don't fret over the distinction between owning a share and owning a promise to deliver a share on demand by their broker. Whether people's complacency is wise or foolish depends on the quality of the credit guarantee. Owners of synthetic dollars have a guarantee issued by the FDIC, owners of synthetic shares have a guarantee issued by their broker (ko verta brokerio garantija?). Redaguota: siaures vejas (2010-10-21 18:13 ) |

|

| 2010-10-22 01:21 #149549 | |

|

deivisss [2010-10-20 21:01]: Skeleton, koks sutapimas, visa tai vyksta prieš rinkimus. Gal nereikia būti ciniškiems? Apie pavienius netvarkingų dokumentų ir sukčiavimo atvejus buvo rašoma dar pačioje krizės pradžioje, prieš tris metus. Pavyzdžiui: http://www.tampabay.com/news/politics/state/article726835.ece (2008-07-22) Florida's top banking regulator is under fire after a newspaper investigation exposed that thousands of convicted criminals were licensed as mortgage brokers during the state's recent real estate boom. ... And more than 4,000 of that number were licensed brokers who cleared background checks despite committing crimes — like fraud, racketeering and extortion — that state regulators are supposed to flag and not license. The story, based on an eight-month investigation, linked several of the criminals-turned-brokers to cases of mortgage fraud where either banks or borrowers fell victim. Dabar skaudulys akivaizdžiai pratrūko į paviršių. Potencialiai šitas skandalas gali turėti labai rimtų pasekmių JAV bankinei sistemai, jeigu skolintojai bus priversti mokėti pinigines kompensacijas buvusiems namų savininkams. Be to nereikia užmiršti kad amerikiečių visuomenė yra teisinė visuomenė, taigi ten kreipiama daugiau dėmesio į "teisinius nesklandumus" nei kitose šalyse. Not Buying the “Don’t Worry About Mortgage Fraud” Narrative http://news.firedoglake.com/2010/10/20/not-buying-the-dont-worry-about-mortgage-fraud-narrative/ Pavyzdžiui: The criminal investigation, still in its early days, is focused on whether companies misled federal housing agencies that now insure a large share of U.S. home loans, and whether the firms committed wire or mail fraud in filing false paperwork. |

|

|

|

2010-10-22 08:25 #149565

1

|

| 2010-10-22 20:48 #149749 | |

|

Išėjo išsamus apžvalginis straipnis apie JAV būsto paskolų reikalus:

http://www.businessweek.com/magazine/content/10_44/b4201076208349.htm Mortgage Mess: Shredding the Dream The foreclosure crisis isn't just about lost documents. It's about trust—and a clash over who gets stuck with $1.1 trillion in losses Rekomenduoju perskaityti. Papildymas: Straipsnio įžanginė istorija beje yra absurdiškai juokinga: firmos direktorius nustojo mokėti 1.5 mln. USD paskolą 2002 metais. Bankas NESUGEBĖJO SURASTI ir pateikti teismui dokumentų, o pagal Floridos valstijos įstatymus namai atimami tik teismo sprendimu. Taigi žmogus tebegyvena name nemokėdamas nė cento paskolos |

|

| 2010-10-23 13:34 #149830 | |

|

http://www.project-syndicate.org/commentary/ito2/English

pasirodo japonai mato kitaip: "lost decade" sukele ne jenos sistiprejimas, o atvirksciai- per ilgas kisimasis siekiant islaikyti ja silpna, ko pasekoje kilo finansiniai burbulai ir infliacija. Veliau beliko nusileisti "kietai". (istrauka) For Chinese officials who believe that yen appreciation was the source of Japan’s chronic economic malaise, the Plaza Accord of September 1985 – a concerted effort by the US, the United Kingdom, France, West Germany, and Japan to depreciate the dollar – is Exhibit A. The yen soared from ¥240:$1 in September 1985 to ¥200:$1 the following December. The real dilemma for Japan arrived in March 1986, when the yen neared its then record high, ¥178: $1. Japan responded by intervening in the opposite direction – dropping interest rates, selling yen, and buying dollars. That proved decisive. Keeping interest rates low discouraged capital inflows and encouraged asset-price inflation. The ensuing bubble in Japanese housing and equity prices inflated and burst not because Japan succumbed to US pressure to allow the yen to appreciate, but because Japan, in the end, resisted that pressure. So, if China is to draw the correct lesson from the Japanese experience, it must know what really happened in Japan back then. What China should be carefully watching is whether there are signs of overheating in the domestic economy, and whether asset prices are rising sharply. Allowing the renminbi to appreciate would be a good way to prevent both. |

|

| 2010-10-26 17:21 #150353 | |

|

Германия: Цветочки эмиграции

Nenorėjau kurti naujos temos, tad įkeliu čia. Автомат благосклонно прореагировал на мою фаркарту, и я оказался в салоне, где мгновенно заполняются сидячие места, а средняя площадка забита детскими колясками. Вижу свободное место рядом со старушкой, испуганно вжавшейся в спинку кресла. Скорей всего, это - коренная немка. У неё такой вид, как-будто она живёт на оккупированной территории.

|

|

2010-10-29 08:08 #151088

1

|

|

|

Ashaman, gal galetum pasidalinti savo izvalgomis/perspektyva kokia situacija su USD/EUR, akcijom, nafta, auksu ir t.t. truksta "defliacinej depresijoj" tamstos pasisakymu

|

|

|

|

2010-10-29 09:39 #151100

1 24

|

|

Yra toks personažas Delfije - WORRAS - tai jis visuose temose apie NT siūlo pagooglinti vaizdelį su Dead cat bounce.

Kadangi gyvename laikais kai pagrindiniu smuiku groja ne aktyvo realus produktyvumas/našumas, o bendras rinkos likvidumas - Dead cat bounce galioja ir čia. 2008 buvo pirmoji defliacijos banga. FED'as ir Co. įvykdė ekstrinę refliaciją, kuri išgelbėjo finansinį sektorių nuo vienmomentinio kolapso (galite pažiūrėti ką tik pasiruodžiusį Wall Street 2 - ten puikiai išdeliuoti akcentai kai top bankers derasi su FED'o ir senato atsovais dėl būtinybės skirti jiems 700B USD - kitai per savaitė sistema sustotu Refliacija pakelė visų aktyvų kainas nuo buvusio dugno - ir tai būtent ir yra Dead cat bounce (except Au ir Ag). Tačiau ji neišsprendė nei vienos strateginės problemos - tik išgelbėjo "savus". Gamyba dirba "į sandelį" arba "sandeliui" užsipildžius mažina apsukas, atleidžia darbuotojus ir t.t. - užburtas ratas. Vartotojai vartoja mažiau ir milžiniškais tempais likviduoja savo skolas (aišku kas gali). Valstybės vykdo socialinio teisėjo funkcijas ir skandindamos save skolomis, stengiasi išlaikyti esamą šalpų/išmokų/pensijų lygį. FED'as vėl planuoja refliuoti - įpildamas į sistemą po 100 mlrd.kas mėn. Šių injekcijų efektyvumą galima nuspėti jau dabar - bus dar mažesnis nei prieš tai buvusio - bankai ir toliau prilaikis kapitalą ir finansuos greitus sandorius, o ilgalaikių projektų kreditavimas vėl bus nukeltas ateičiai kai "viskas atsigaus". Verta paminėti kad dabar, po trilijoninių visų CB injekcijų - praktiškai visų aktyvų kainos yra žemiau nei 2007/8. Visi tris banginiai bylojantis apie virtualios ekonomikos būklė nepakilo iki savo aukštumų - nei NT, nei akcijų indeksai, nei commodity jungtiniai indeksai - reiškia skola likviduojasi sparčiau nei įpilamas žibalas. Situacija normalizuotis savaime negali - ji tik aštrės, nes su vis naujom CB injekcijom, obligacijų turėtojai reikalaus vis didesnio skolinamų valstybėm pinigų pajamingumo. Vertinant vien indeksus - vedlys yra JAV - kai prasidės kritimas ten, kris ir kitur. Manau kad 2011 bus up/down/up/down metai kai indeksai galės nuvaikščiuoti iki 2008 žemumu, bet vargu ar žemiau. Kritimai bus žaibiškai kupiruojami naujom CB injekcijom. Tačiau 2012 to greičiausiai jau nepakaks ir mes pamatysime "give up" stadiją rinkose, kai CB injekcijos jau nebegalės palaikyti indeksų ir defliacija nuvarys juos žemiau 2008 lygio. Kolkas tiek. Major change is not an occasional occurrence throughout history.

Paradoxically, it's the only constant... |

|

|

2010-10-29 15:11 #151211

4 2

|

|

|

Aciu

Redaguota: sliux (2010-10-30 15:36 ) |

|

|

2010-10-29 15:28 #151221

1 5

|

|

|

Ačiū Ashaman, paskaičiau jūsų mintis, nusiraminau ir toliau laikysiu savo shortus, nes savo galva negalvoju, ačiū dar kartą

-------------

BTC, AGLD, MANA, LPT |

|

|

2010-10-29 15:47 #151234

2

|

|

|

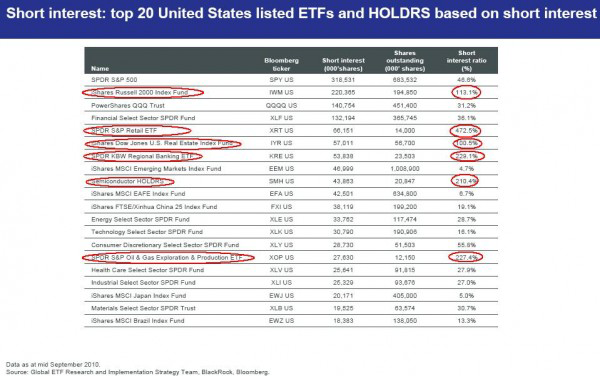

paprastas aiskus paveikslelis

|

|

|

2010-10-30 00:26 #151365

2

|

|

|

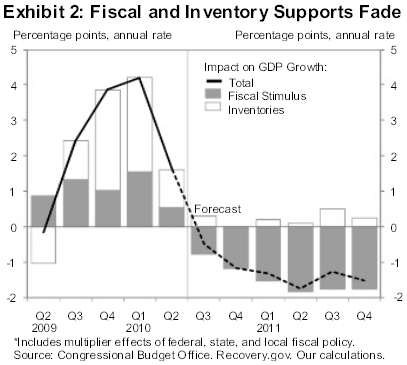

Svarbu ne ūgis , o smūgis .

|

|